Ultimate guide to private pension plans in Germany

Compared to other EU countries, Germany offers you tax incentives when you invest through private pension plans.

Table of contents

- 1. What is a private pension plan, and why does it matter?

- 2. The three main private pension plans in Germany you should know

- 3. What are the common misunderstandings surrounding private pension plans?

- 4. Private pensions and ETF investments

- 5. FAQs

What is a private pension plan – and why does it matter?

As you may be aware, the public pension you will receive from the government won’t be enough to maintain your lifestyle. This problem is very acute in Germany, where the government only commits to covering 50% of your income when you retire.

You might even already be investing in something long-term, including stocks, property or ETFs. (Don’t worry if you don’t know what an ETF is yet – we’ll explain what it is in the article).

So, why should you care about private pension plans?

The answer is simple – tax benefits!

Private pensions are incentivised by the government by granting you specific tax benefits if you invest through a private pension plan.

We have put together this ultimate guide to private pension plans in Germany. It covers everything you need to know about private pension plans in Germany, what pros and cons are, and which one is right for you.

So – what is a private pension plan?

Essentially, a private pension plan is an investment contract offered by private investment firms that qualify for special tax treatments. It is used as an additional pension to your existing public pension. You have the final say over what the investment contract specifically invests in.

“A private pension plan is an investment contract that gives you an additional pension on top of your public pension”.

Investing in private pension plans vs. ETFs

What is an ETF?

ETFs are stock-listed funds. They allow you to invest in the stock market in a cost-efficient way, typically following well-known indexes such as the DAX, S&P500 or Nasdaq.

Why does it matter for private pensions?

ETFs are commonly accepted as one of the most reliable high-return long-term investments.

Almost every private pension provider in Germany allows you to invest in ETFs through private pension plans.

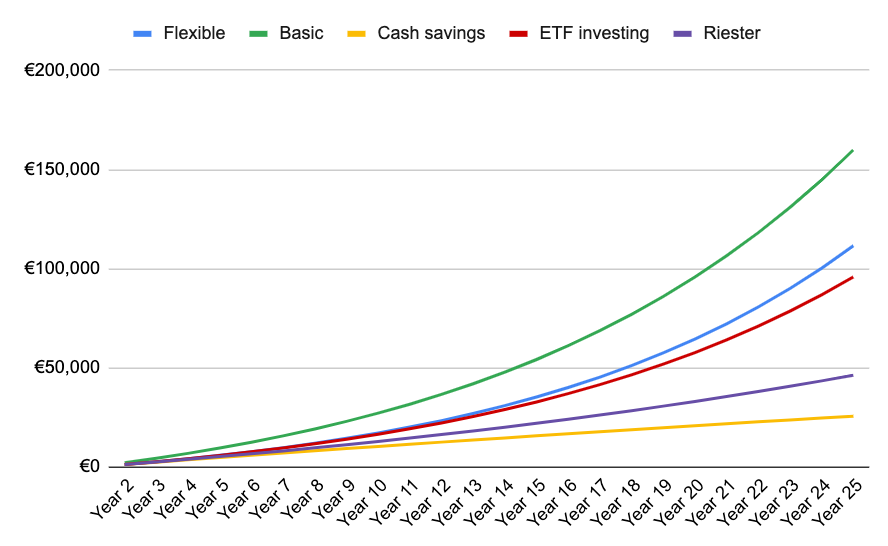

Here is how €100/month netto (after tax) salary investment in the S&P500 looks like with various pension plans:

Below we will highlight the three main types of pension plans and highlight which ones allow you to invest in ETFs.

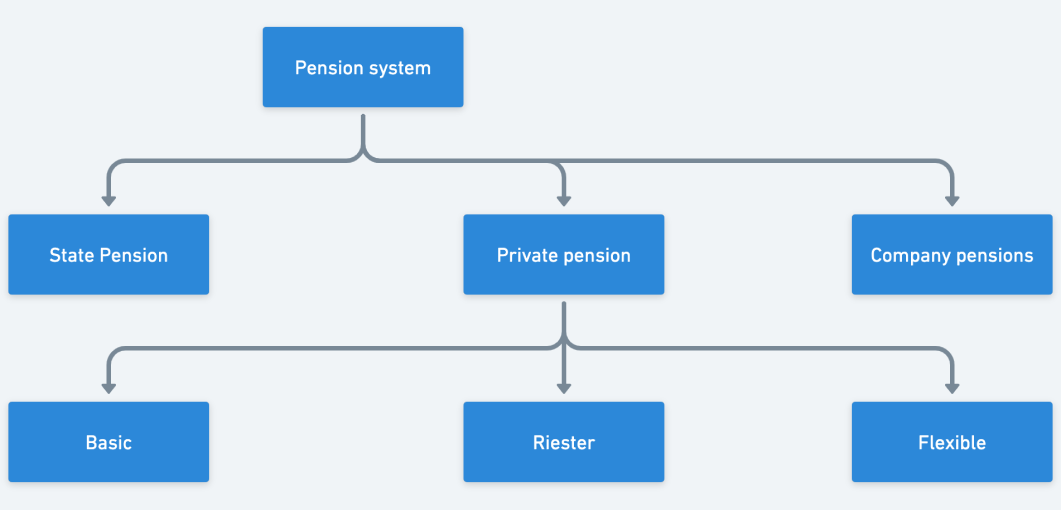

The three main private pension plans in Germany

There are three main private pension plans in Germany with tax advantages. They all have different conditions and benefits respectively.

#1: The basic pension (commonly known as Rürup)

Originally created for the self-employed (who get no public pension whatsoever in Germany), the basic pension plan can be used by anybody working in Germany. It is a voluntary scheme where you invest from your brutto (pre-tax) income.

Little known is that while pension contributions increase with salary, your acquired state pension does not increase in line as much.

This leaves many high-income earners unpleasantly surprised when they retire as their state pension is significantly less than they expected.

What are the advantages of the basic pension in Germany?

The main tax benefits while you work

- Tax benefit 1: Defer income tax

The basic pension is a deferred income tax scheme which means that the government agrees to not tax your contributions this year. Rather, your income is taxed when you retire instead.

This exists in many EU countries, and it is a common way for states to incentivise their citizens to put money aside for their retirement.

This is only on the condition that the money you put into such a scheme can only be taken out at retirement.

Essentially, you are not allowed to take the money out before the age of 62 – the investments have to be converted into a lifelong income (annuity).

There is still a small loophole which some EU countries exploit, however, allowing you to enjoy the basic pension returns and retire in an EU country with low tax (Hint: Portugal, for example). - Tax benefit 2: No Capital Gains Tax

Normally, the government applies taxes to any profit you make on your investments.

This is called capital gains tax.

If you invest in a basic private pension plan, you are not liable to pay any capital gains tax when you work.

This is significant as it allows you to reinvest your capital gains – and gain upon those gains. This principle is called “compounding” and forms a powerful dynamic for creating wealth.

- Tax benefit 3: No Dividend Income Tax

Some investments also pay out income in the form of dividends which are taxed at 25%. Private pension plans allow you to receive this money and automatically reinvest it without incurring dividend income tax. - Tax benefit 4: Changing your investment strategy without incurring taxation

Normally, when you balance your portfolio or make adjustments in your investment strategy, you have to sell and reinvest into different funds – triggering taxation.

When you invest in your retirement plan, however, you can either have the investment provider automatically re-balance your portfolio – or you can take out a self-managed plan where you can do this yourself.

In any case, you can freely change your investment strategy. There are many strategies you can agree on with the pension provider. An example is the managed three-fund (Drei-Kopf) strategy which allows you to shift your money between two funds (Zwei-kopf) and exit all investments during periods of high market uncertainty.

Ability to invest in high-return ETFs

The government does not impose strict restrictions on the basic pension plan and allows you to invest in any investment portfolio, including ETFs as well as a portfolio of ETFs.

Read more about ETF investing with a private pension

Additional benefits of the basic pension plan

- Retiring abroad

Interestingly, you can defer income tax in Germany and retire abroad (say, Portugal) where you pay a lower tax on your pension income.

This doesn’t work for countries with no tax, however, such as the UAE.

This is because the German government has the ability to apply its taxation on private pension plan contracts – just in case you go and live in a country where you pay no tax at all.

Either way, it is important to check if there are dual-tax agreements between Germany and the countries you might be considering retiring in.

- Does the basic pension plan give me guarantees?

Yes, you can also have guarantees in a basic pension, but do keep in mind that this will lower the return on your investment in return for the additional security. - Mixed portfolio investment strategy

There are no considerable limitations in what you can invest in through a basic pension. - How does inheritance work?

The basic pension itself is not directly inheritable. However, you can nominate your legal partner who will receive your pension for a set period after you pass away. This period can be adjusted to your personal and family’s preferences depending on the agreement with your provider.

What flexibilities do I have with the basic pension plan?

A basic pension plan still gives you a lot of control over your investments. This includes:

- Selecting your own investment portfolio (including any ETF investments)

- Choosing to have guarantees (albeit not necessarily recommended)

- Pausing, resuming and adjusting your investment at anytime

How can I claim the relevant tax benefits?

To take advantage of the tax benefits, you have to set up a basic pension plan first. Once that is done, you can start contributing into the plan.

When you make a tax declaration, you need to tell the government the amount you contributed to the basic pension plan in a certain year. They will take this into account when calculating your final taxation.

In most cases, you will receive a refund for the money that your employer already paid to the government. If your tax situation is complicated in nature, you might need to double-check with an accountant.

Basic pension plan: Summarised

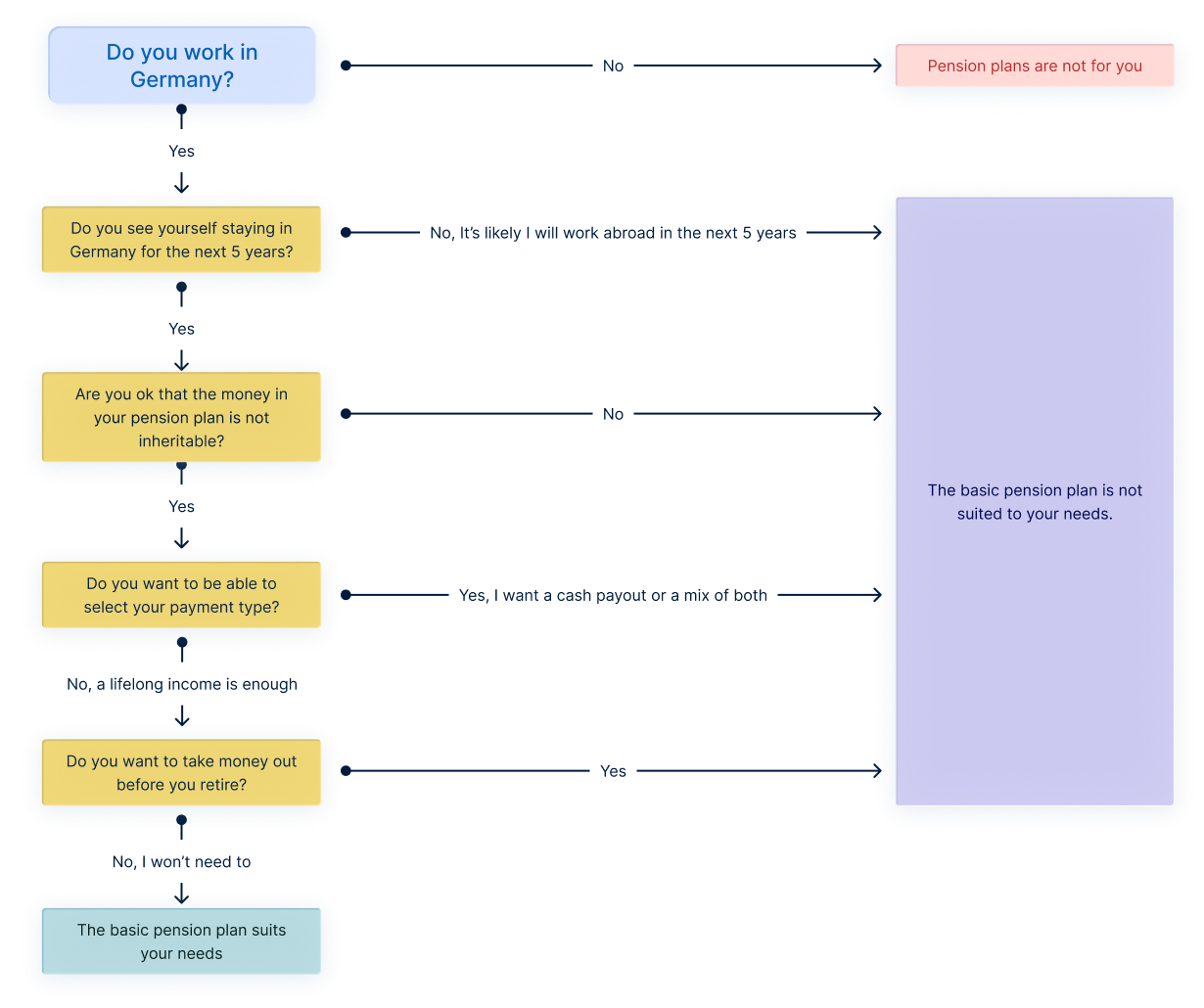

A Basic pension plan is best suited to anyone living and paying taxes in Germany, and that are likely to do so for the next 5 years. If this fits your situation, this plan will see the highest return on investment.

Who is it for?

- Everybody who pays income tax in Germany

- Those who are ok with receiving the money as a lifelong pension, rather than a lump sum

- You are not likely to be working abroad in the next 5 years

Pros

- Tax shield from capital gains tax

- Tax shields from dividend income tax

- Tax-deductible contributions from income tax

- No restrictions on investment funds

- Stop, change or pause contributions anytime

- Acquire the pension to retire abroad

- Lifelong income guarantee

- Your income can be inherited by a designated partner

Cons

- Has to remain invested in until you are at least 62

- Certain tax advantages only apply if you invest while living in Germany

- No option to pay out capital lump sum

- Money is not inherited directly

- Not suitable if you are planning to work abroad in the next 5 years

Is the basic pension plan for me?

You are able to combine several pension plan types, which is seen as a better option than investing your capital into one item.

Check basic pensions available to you

Find out which basic pension plan is right for you on our comparison portal.

#2: The flexible pension plan

The flexible pension plan is for those who want to be able to retire abroad or those who want to be able to access their money before the retirement age is reached.

However, as there is no commitment from your side to only secure the investment for your retirement, the German government does not give you income tax relief on your investments.

That said, there are still tax benefits to a flexible private pension.

What does the flexible pension plan have in common with the basic pension plan?

The following points are something we have touched upon above. They are:

- You can invest in high-return ETFs

- You can retire abroad

- Both shield you from capital gains tax

- Both shield you from dividend income tax

The key difference from the basic pensions is that you gain flexibility in return for fewer tax benefits.

- The basic pension allows you to defer income tax

- The flexible pension allows you to take the money out at any point in time. The basic pension plan does not

The key difference between the basic and flexible pension plan is that flexible pension plan gives you more flexibility in return for less tax benefits.

What flexibilities do I have with the flexible pension plan?

With flexible a private pension plan, the clue is in the name. Your flexibilities include:

- Selecting your own investment portfolio

- Choosing to have guarantees (albeit not necessarily recommended)

- Cancelling, pausing and adjusting your investment at anytime

- Say over when and how you take the money out

- Nominate an inheritor if you choose

Flexible pension plan – the main tax benefits while you work

Just like with the basic pension, you are investing through a private pension contract and therefore you are not incurring capital gains tax and dividend income tax as you do not hold the investments directly.

This allows you to switch your investments around, sell, reinvest them and receive payments from your investments – without having to pay the government a share of the profit.

This can be used to reduce taxes on popular investment strategies such as ETF investments, ETF savings plans and dividend-paying investments. Some contracts can be setup with an active strategy such as moving the money into safe investments when the market goes down (Zwei-kopf) – and even taking out all investments for some time when the market is uncertain (Drei-kopf).

This property is typically called a tax shield, but you may have heard of it also being referred to as a tax wrapper.

Summarised, these points boil down to:

A flexible private pension plan is a tax wrapper for existing ETF investments. It gives you a tax shield against capital gains tax and dividend income tax.

Flexible pension plan – the main tax benefits when you take the money out

If you take out all the money after the age of 62 as a lump sum, you qualify for a special tax rule that is usually more tax-efficient. It means that:

- Your original contributions (capital) are not taxed

- Your gains on your contribution (capital gain) are taxable by the state but only 50% of your capital gain is taxable

- The state taxes this reduced amount as income tax

- While the income tax rate is higher than the capital gains tax, the end result is typically less than if the entire capital gain were been taxed as capital gains tax.

However, the flexible private pension allows you to pay out the lump sum in multiple tranches which means you can avoid the higher income tax rates by spreading out your lump sum payment over several tax years.

Another advantage for you: If you opt for lifelong income instead, the amount of the pension you are taxed is fixed to your retirement age.

For example, if you retire at the age of 63, you pay income tax on 20% of your pension. If you retire at 77, you pay income tax on only 10% of your pension.

You can find a full detailed list regarding the ages and percentages here.

Important: You can only reap the rewards of tax benefits with the flexible pension plan if:

- You are 62 years of age or older

- Have had a flexible pension contract in place for at least 12 years

The following only applies when you take out the money as a lump sum. Please note that different countries implement different tax rates.

You can cancel your flexible pension contract before you reach retirement age. However, this means that you will pay capital gains tax on all the gains you made. If you frequently adjusted your portfolio while investing in your flexible pension plan, you are still able to make gains, albeit much smaller.

Flexible pension plan: Summarised

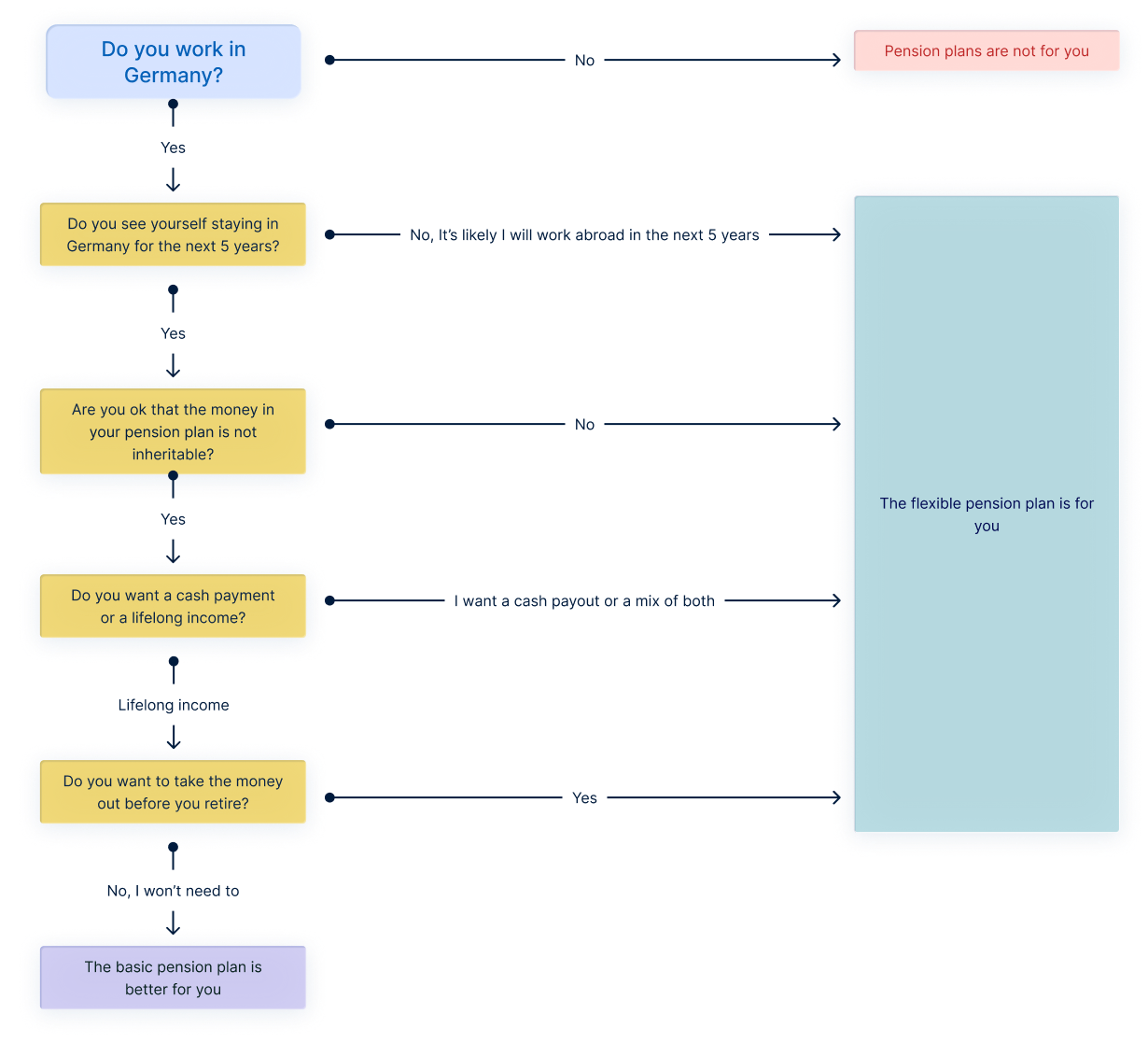

A flexible pension plan is suited to anyone that is not willing to lock in their money until the age of 62 or people who want to take out all the money at once when they are retired.

Who is it for?

- People looking for the option to retire abroad

- People considering working abroad in the next few years

- People of all income levels

- People not looking to commit to an investment which binds them until they are 62 years old

Pros

- Tax shield from capital gains tax

- Tax shields from dividend income tax

- Can be cashed out anytime

- No restrictions on certain investment funds

- Stop, change or pause contributions anytime

- Acquire the pension to retire abroad

- When cashed out on retirement age only 50% of the capital gains are taxable, but they are taxed as income (rather than capital gains)

- Can be converted into a lifelong guaranteed income

- Can be taken out as lump sum

- Your income can be inherited by a designated partner

Cons

- Has to remain invested in until you are at least 62 to receive the 50% tax reduction

- Need to be invested in for at least 12 years to qualify for the 50% tax reduction

- Contributions are not tax-deductible

Is the flexible pension plan for me?

Note: You are able to combine several pension plan types, which is seen as a better option than investing your capital into one item.

Check flexible pensions available to you

Find out which flexible pension plan is right for you on our comparison portal.

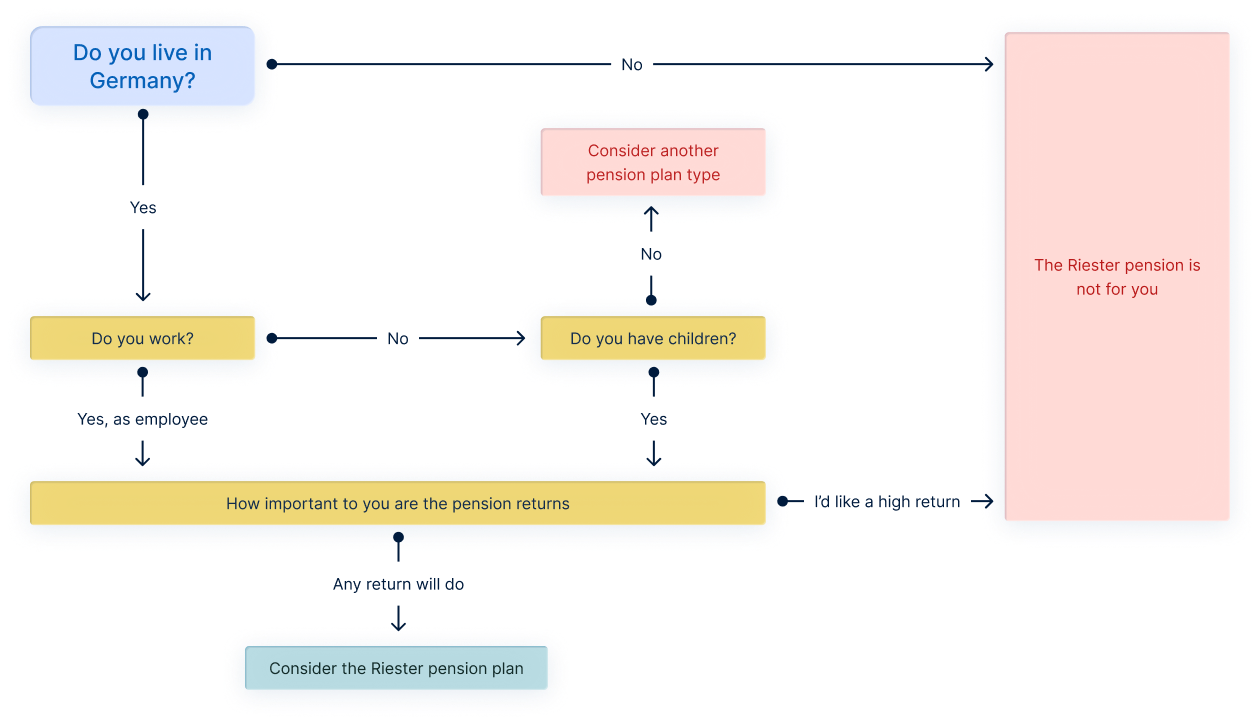

#3: The Riester pension

Ask any German and you will undoubtedly hear something along the lines of “Riester sucks”, which is generally true to the point that most providers stopped offering them.

The Riester pension is best suited to low earners and large families.

How does it work?

By regulation, the Riester pension guarantees that you will have 100% of your investment back at the end of the contract, which doesn’t sound like a hard thing to achieve. However, since investing is highly uncertain, the only way to achieve this level of certainty is to invest in very safe, low-return investments.

As the Riester is designed for low-income earners, the government subsidises this private pension with grants.

Tax benefits while you work

The main benefit of the Riester pension plan is that the government adds a contribution of €175 per adult and up to €300 per child per year. This is beneficial for large families and people who are not able to save much on their own.

As with the other plans, you are able to invest tax-deductible up to €175 per month. The gains are tax shielded from income dividend tax and capital gains tax.

However, the Riester pension plan only receives subsidies as long as you are based in Germany.

Riester pension: Summarised

A Riester pension plan is considered to be safe, yet low-return investment plans that guarantees a 100% return on your contributions. It is only suited to those who absolutely need their money guaranteed.

Who is it for?

- Large families

- Unemployed

- Low-income earners

Pros

- You are guaranteed 100% of your investment back

- You get a tax-deductible investment of €175 per month

- Government pays up to €300 per child per year

- Government pays in €175 for yourself

Cons

- Low return due to restricted investment regulation

- Cannot move to a non-EU country to keep the Riester contract.

- You are supposed to use the money solely as lifelong income

Is the Riester pension plan for me?

Note: You are able to combine several pension plan types, which is seen as a better option than investing your capital into one item.

What are the three most common misunderstandings about private pension plans in Germany?

Misconception 1: The investment options are too limited

Private pension plans used to be very constrained in what type of investments were possible. The state had strict guarantee requirements, and many people still hold this misconception.

Luckily, this is no longer the case.

You may still see more traditional ones, such as the appropriately named classic pensions.

These haven’t performed well in the past decades, resulting in expensive guarantees and high costs for those taking out contracts. Classic pensions are to be avoided.

Modern private pension contracts act as wrappers around existing fund investments, such as ETFs.

The most modern private pension providers allow you to select from 100s of ETFs, many of which have performed very well in the past few decades, often with 10% annual returns.

“Modern private pension contracts act as wrappers around existing fund investments, such as ETFs.”

What else do I need to keep in mind?

It is important to find a provider who offers you a wide selection of investment funds that doesn’t add management fees (AUM Fee) on top.

If you’ve made ETF investments already, you can easily continue your existing portfolio strategy with your private pension contract.

Request a free consultation

Our experts take great pride in answering any question you may have

Misconception 2: The costs are too high

As we mentioned above, classic pensions are very expensive due to the guarantees they had to provide. However, this is no longer needed for modern private pension plans. As a result, you have much cheaper alternatives.

There are many private pension providers, and their competition is good news for you: As they compete with one another, there are more and better plans available to you to choose from than in recent memory.

While the administrative costs are usually more expensive than investing directly in ETFs (due to the regulatory and tax compliance obligation of the investment firm), your potential tax benefits greatly outweigh the initial fees.

This is true for all types of private pension plans. But more specifically, this case is strongest with a basic pensions plan, where your entire investment is tax-deductible to the point that you can get up to 40% of your investment back as a tax refund.

Is the capital gains tax a problem for private pension plans?

No. Luckily, investing in a private pension plan will avoid you falling to the same fate entirely.

You won’t be liable to pay tax on your investments – as long as you do not take the money out. Meanwhile, you can adjust your investment strategy as you see fit at any time.

This property has many names but often it’s called a tax shield.

In summary, is a private pension plan expensive?

It doesn’t have to be. Private pension plans are often a cost-effective way to invest due to the tax advantages you can benefit from.

Misconception 3: Stocks have better returns

When you earn dividends or sell stock market investments, you trigger taxation.

When you hold investments directly, and you want to move money from one investment into another, you are practically selling the investment. Therefore, you have to pay tax on the realised gain.

However, if you hold investments indirectly through a private pension contract, technically, your gains are never officially realised. Therefore, you aren’t liable to pay any capital gains tax.

How do you know if you are holding the investment directly?

- You are investing in ETFs with a depot such as Scalable Capital, Trade Republic or others

- You are investing in ETF savings plans

- You are investing with an automated portfolio manager (also known as robo-advisors)

- You hold stocks directly

Capital gains tax has caught out many inexperienced investors when self-managing their portfolios. They cannot be avoided as the Finanzamt (tax office) exchanges data with German investment platforms.

In summary, are private pensions low-return investments?

They are only low if you select low-return investment funds, such as a government bond fund.

Private Pension Plans with ETF Investments

What is an ETF, and why is it relevant?

As we mentioned throughout the article, an ETF is an acronym for “exchange-traded funds”.

Investment researchers have long observed that passive, highly diversified investments often outperform actively managed funds in the long run.

This gave rise to ETFs.

They are automated, with no manager directly overseeing, meaning they are low-cost.

The most well-known ETFs usually track a basket of stocks, such US Technology firms, or the S&P500 (the 500 biggest companies listed on stock exchange in the USA).

They are regarded as a great way to invest due to the stock market’s generally high performance over the last 30 years.

The most common advice online is to invest in ETFs long-term. This is why private pension providers are now competing with one another to provide ETFs to their portfolios.

Providers with more than 200 ETFs are common and have become market standard.

Request a free consultation

Our experts take great pride in answering any question you may have

“An ETF is an acronym for “exchange-traded fund” and is used to invest highly diversified in the stock market.

Investing in ETFs through a private pension plan

Private pensions have tended to prevent you from investing all your capital in the stock market – but this is no longer true.

Now, you can combine the benefits of ETF investment with the tax benefits of private pension plans.

Private pension providers have also caught up with the trend of Savings Plans incorporating ETF investment into their model. They allow you to build your own portfolio and make regular investments.

While investing directly in ETFs isn’t particularly tax-efficient, they have their benefits (depending on the situation).

When is it better to just invest in just an ETF?

If you invest for a financial goal that happens before you retire, such as sending your children to university, or using the money invested as a down payment for a house, ETF investments are a suitable option for you.

However, you shouldn’t invest all of your emergency cash reserves into a private pension. As we mentioned, you are able to cancel a flexible private pension plan at any time. However, you will pay penalties if you do so.

When can it be better to just invest in just a private pension plan?

The short answer: For your retirement.

If you use an ETF investment for your retirement, you are paying more taxes than necessary. A basic pension plan as well as a flexible pension contain tax advantages for your retirement, meaning you save money long term.

Investing in ETF-based private pension plans with income tax deferral allows you to invest up to €166 for every €100 that you would have invested in an ETF savings plan instead.

In the best case scenario, a private pension plan can see you gain up to 66% more of your investment than just with ETF investments.

Looking for a private pension plan?

Visit our comparison portal and find out which plan is best-suited to you.

FAQs

Our frequently asked questions about private pensions plans in Germany.

How many private pensions can you have?

Will the use of multiple private pensions is doubtful, there is no limit regarding the number of contracts you have. You can also invest as much money as you want.

Does my private pension follow if I move jobs?

Since a private pension is a completely private contract, it is fully independent of your employment or workplace.

Do private pensions increase with inflation?

This depends on the investments you choose for your pension. Some, like bonds, will not grow. While others may profit from inflation.

Can I transfer my company pension to a private pension?

No, a company pension and a private pension are distinct and cannot be converted into each other. However, you have the option to supplement your company pension with personal contributions if you so choose.

Can I take a lump sum from my private pension?

Yes, this is always possible. To use the tax benefits, however, it would be necessary to own the private pension plan for more than 12 years and wait for the payout until you are 63.

Can I sell my private pension?

That is not directly possible. But you can quit the private pension contract and receive the capital as an immediate payout.

Can I have a private pension and a company pension?

Without a problem! While both serve the same purpose, they do not hinder each other and be used at the same time. There are no negative consequences to do so.

What happens to my private pension if I move abroad?

This is not a problem. If you move to another country, you can still use your private pension and get paid later. But, you should be careful about taxes in your new country.

How to get a private pension?

In Germany, most insurance companies and banks offer their own version of a private pension. But it would be good to talk with a dedicated financial advisor first, like Horizon65!

Can I withdraw my private pension early?

Yes, it is possible to withdraw your private pension anytime. However, you may lose some of the tax benefits. It is also possible that you will have to pay some of the cost, your pension caused for the provider.

Are private pensions safe?

A private pension can be invested however you want. This may include risky assets, if you choose so. Such a pension is of course not completely secure. But it is equally possible to have a very secure investment, with guarantees given by the provider. The decision is yours.

Can I withdraw my private pension before 55?

Yes, in Germany it is possible to receive the pay out of your private pension insurance early. However, you will miss out on a few tax benefits.

What happens to my private pension when I die?

This depends on the actual contract. Generally, however, the money still contained in the contract is added to the estate and paid out to the heirs.

Can I take my private pension and still work?

As a completely private contract, your private pension is in no way dependent on your work or retirement. If you work or not is of no concern for your payout.

Does a private pension affect your state pension?

No, there is no relation between the private pension and your state pension.

What is pension insurance

<span style="font-weight: 400;">A pension insurance is an investment contract. You invest your money and in return, you will receive a pension in old age or have the ability to take a lump sum payment on retirement. The exact conditions of this arrangement can vary widely, from management fees, to investment strategy, to how the money is used to provide you with a replacement income. We recommend you speak to our advisors before contracting such an insurance, you can book an appointment with them in our app.</span>

How much should you invest in your retirement plan?

This depends on how early you start investing. If you are building up your retirement savings, you should set yourself a clear goal with a realistic amount that you would like to have later in your old age. It is important to be honest with yourself and take into account all costs (both fixed costs and costs for leisure activities and unforeseen costs). You should also remain realistic when assuming the development and rather set the value development somewhat lower. This is the only way to prepare well for your retirement. We can help you to clarify this difficult question and to design an optimal solution with you in which your investment is as low as possible in order to still achieve your goals. Make an appointment with our pension experts.